At 72, most Americans are already a few years into retirement, navigating a financial landscape shaped by decades of saving, spending, homeownership, and the occasional market shock. The question of how much wealth they’ve actually accumulated is one that many people wonder about quietly, whether they’re approaching that age themselves or just trying to figure out if their own trajectory makes any sense.

The honest answer is that the numbers vary enormously, and the gap between the typical 72-year-old and the average one tells a story worth understanding. What looks like a comfortable national average often masks a much more uneven reality underneath.

The Average vs. the Median: Two Very Different Stories

The Average vs. the Median: Two Very Different Stories (Image Credits: Unsplash)

While average net worth is useful to know, median net worth by age tends to be more representative of where Americans actually stand. That’s because the median reflects the 50th percentile of earners, while the average factors in outliers with very high or very low net worths. For people in their early 70s, this distinction is especially significant.

Net worth begins to decline gradually once Americans enter their 70s, and median figures are far lower than averages, highlighting how a relatively small number of high-wealth households can skew the results considerably. Understanding which number you’re looking at changes everything about how you interpret the data.

What the Federal Reserve Data Actually Shows

What the Federal Reserve Data Actually Shows (Image Credits: Unsplash)

According to Federal Reserve Survey of Consumer Finances data, the highest average American net worth belongs to those aged 65 to 74, sitting at $1,794,600. By contrast, Americans 75 and older show an average net worth of $1,624,100. At 72, most people fall squarely in that 65 to 74 bracket, which represents the peak of average accumulated wealth in America.

U.S. Census Bureau data on household wealth found that for households in which the head of household was between 70 and 74 years old, median household wealth was $403,000, or about 2.3 times the value of overall median wealth. That’s a meaningful figure, but it’s a long way from the headline average that often gets reported.

Why the 65–74 Age Group Peaks in Wealth

Why the 65–74 Age Group Peaks in Wealth (Image Credits: Unsplash)

People ages 65 to 74, whether just retired or fully settled into retirement, tend to have the largest net worth of any age group, thanks to assets increasing in value over a long period of time and the fact that many have paid off their homes. The vast majority, about 77 percent, of people ages 65 and older own their home. Homeownership plays an enormous role in that wealth accumulation story.

In general, as Americans age, their net worth increases. Over time, people are able to command higher salaries and purchase property, while their investments and retirement accounts continue to grow. For a 72-year-old, that means decades of compounding have already done significant work, for better or worse, depending on the choices made along the way.

The Role of Home Equity at Age 72

The Role of Home Equity at Age 72 (Image Credits: Unsplash)

For many retirees, home equity is their largest single asset. The median home value for retirees aged 65 to 74 is about $320,000, and nearly 80 percent of Americans over 50 own their homes, with more than half carrying no mortgage at all. That’s a substantial cushion, though it’s one that isn’t always easy to access without selling or borrowing against the property.

For those at the 25th percentile of net worth in the early 70s age group, total net worth reaches roughly $125,000. At the median, total net worth peaks near $439,000 in the early 70s, though investable net worth, excluding home equity, is closer to $238,000. For many households, the home is doing the heavy lifting while liquid savings remain comparatively modest.

Social Security and Income at 72

Social Security and Income at 72 (Image Credits: Pexels)

Social Security is often called the foundation of retirement income in America, and for good reason: roughly 40 percent of older Americans rely on it for at least half of their income, and 15 percent depend on it entirely. For a 72-year-old who claimed benefits at the optimal time, monthly payments can be substantial. For those who claimed early, the picture is leaner.

Waiting until age 70 to claim Social Security can increase monthly payments by roughly 80 percent compared to claiming early at 62, and the delayed retirement credit stops accumulating at 70, making it the optimal claiming age. A 72-year-old who held off until 70 is now benefiting from that patience every month, while those who claimed at 62 locked in a reduced benefit for the rest of their life.

Debt Still Lingers for Many Retirees at This Age

Debt Still Lingers for Many Retirees at This Age (Image Credits: Unsplash)

A surprising number of seniors are still carrying debt that cuts into their net worth. A 2025 LendingTree report found that nearly all U.S. adults aged 66 to 71 had non-mortgage debt, including auto loans, credit card bills, and even student loans, with a median non-mortgage debt of more than $11,000 across the 50 largest metro areas. It’s a number that catches many people off guard.

Debt levels do tend to decline in retirement, but many seniors still carry balances. According to AARP data, the median debt for retirees aged 65 to 74 is about $45,000, dropping to roughly $36,000 for those 75 and older. Those liabilities subtract directly from net worth figures, which means the real spending power at 72 can look different from the asset totals alone.

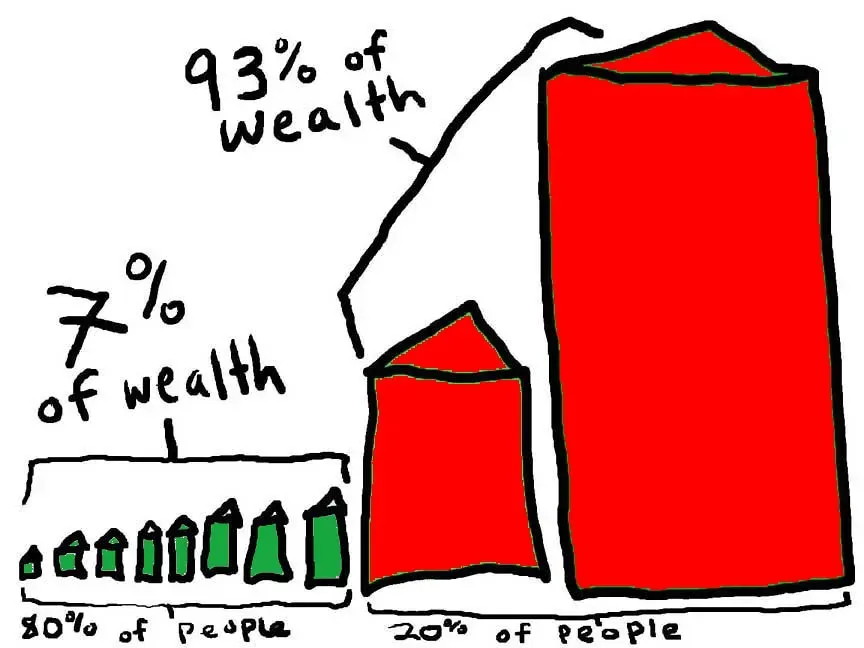

The Wealth Gap Is Wide Even Within This Age Group

The Wealth Gap Is Wide Even Within This Age Group (Sustainable Economies Law Center, Flickr, <a href="https://creativecommons.org/licenses/by-sa/2.0/" target="_blank" rel="noopener">CC BY-SA 2.0</a>)

In 2022, families in the top 10 percent of the wealth distribution held 60 percent of all wealth, while families in the top 1 percent held 27 percent, both figures up significantly from 1989. This concentration doesn’t disappear at retirement age. Among 72-year-olds, the spread between those at the top and those in the middle is striking.

Over the past 60 years, America witnessed a massive transfer of wealth from the middle class to the wealthiest families. In 1963, the wealthiest families held 36 times the wealth of families in the middle of the wealth distribution. By 2022, that figure had grown to 71 times. Many of today’s 72-year-olds lived through that entire shift, and their retirement wealth reflects exactly where they landed within it.

Retirement Account Balances Tell a Sobering Story

Retirement Account Balances Tell a Sobering Story (aag_photos, Flickr, <a href="https://creativecommons.org/licenses/by-sa/2.0/" target="_blank" rel="noopener">CC BY-SA 2.0</a>)

The median 401(k) balance for someone aged 65 or older is $95,425, according to Vanguard data. That figure alone, if withdrawn at the commonly suggested rate of 4 percent annually, would generate less than $4,000 per year in income. Combined with Social Security it can be workable, but it doesn’t leave much margin.

Retirees generally report high levels of financial well-being, but those with income from employment, pensions, or investments are doing substantially better than those who relied solely on Social Security or other public income sources. The source of income matters nearly as much as the amount, and diversification across Social Security, a pension, and personal savings is what separates the financially comfortable from the financially stretched.

How Education and Background Shape Wealth at 72

How Education and Background Shape Wealth at 72 (Image Credits: Pexels)

Higher education is strongly associated with more wealth at this age. Census Bureau data shows that median wealth among households where the most educated member held a high school diploma was $57,020, compared to significantly higher figures for those with college degrees. A lifetime of higher earnings, better access to workplace retirement plans, and stronger investment habits compounds into a very different position by age 72.

Racial disparities in retirement savings are also significant. In 1989, white families had about $50,000 more in average retirement savings than Black families. By 2022, that gap had widened to about $260,000 more than both Black and Hispanic families. These gaps in savings directly translate into gaps in net worth that show up clearly by the time people reach their early 70s.

When Net Worth Starts to Decline After the Peak

When Net Worth Starts to Decline After the Peak (401(K) 2013, Flickr, <a href="https://creativecommons.org/licenses/by-sa/2.0/" target="_blank" rel="noopener">CC BY-SA 2.0</a>)

Net worth generally increases from the 20s through the 60s before declining in retirement, as income falls and assets are gradually withdrawn to meet living expenses. For many 72-year-olds, the drawdown phase is already underway, even if it’s subtle at first. Managing the pace of that decline is one of the central financial challenges of this stage of life.

Aging households eventually draw down their wealth. For households in which the head of household was at least 75 years old, median household wealth was $307,900, roughly 80 percent of the median for those between 70 and 74. That roughly $95,000 difference over just a few years reflects the real-world pace at which retirement savings get spent down, especially when healthcare costs begin to climb.

At 72, the numbers tell a story of remarkable variation. Some Americans are sitting on more accumulated wealth than they’ll ever spend. Others are managing carefully on Social Security and modest savings, relying heavily on a paid-off home as their primary financial anchor. The averages are technically accurate, but the median is what most people actually live closer to, and that number, while meaningfully above the national middle, still leaves less room for error than many people expect at this stage of life.